Guide: Enterprise Risk Management for Financial Institutions

From market volatility and cybersecurity threats to stringent regulatory demands and the complexities of a globalized economy, financial institutions navigate challenges daily that can significantly impact their operations and reputation. This high-stakes environment requires proactive enterprise risk management (ERM) designed for financial institutions.

ERM offers a strategic framework to address these challenges holistically. By integrating risk appetite, risk assessments and risk responses into a cohesive risk management strategy, ERM empowers everyone—from new hires to senior management to the board of directors—to anticipate, evaluate and mitigate risks effectively. This approach ensures alignment across organizational levels, enabling financial institutions to make informed decisions that safeguard stability while fostering resilience in the face of evolving threats.

What Is Enterprise Risk Management?

ERM goes beyond traditional risk management approaches by:

- Identifying and mitigating risks across the entire organization

- Integrating various risk types into a unified framework

- Encompassing ESG, financial, operational, compliance, and cybersecurity risks

Unlike siloed approaches that focus on specific areas, ERM provides a holistic view of potential threats. This comprehensive perspective enables financial institutions to anticipate and address risks proactively, safeguarding both systems and strategic objectives.

Importance of Enterprise Risk Management for Financial Institutions

ERM in the financial services industry goes far beyond mere compliance. Here are a few compelling reasons why:

- Improved decision-making: ERM delivers a consolidated snapshot of potential risks across all domains of your organization. This method allows decision-makers to assess and focus on the most dangerous threats to the business and direct resources to areas with the greatest need.

- Regulatory compliance: Financial institutions follow a tight regulatory structure. They must adhere to rigid criteria to meet industry standards and legal norms. ERM improves compliance by integrating risk management approaches with appropriate industry requirements. In this approach, ERM assists firms in remaining compliant and maintaining a positive market reputation.

- Risk mitigation: Organizations can foresee possible hazards with ERM before they become more severe problems. When you identify threats early, you can establish appropriate controls and processes to minimize these risks. Even in the face of unexpected challenges, this take-charge technique reduces disruptions and financial losses.

- Stakeholder confidence: A solid ERM program highlights an organization’s dedication to transparency and successful risk management practices. It helps build trust with investors, customers, regulators and employees. By proactively managing risks, you can develop stronger relationships and earn the long-term trust of those who matter most.

Benefits of Enterprise Risk Management for Financial Institutions

Implementing enterprise risk management into your financial services organization delivers several tangible benefits:

- Stronger risk culture: Clear policies and training programs help employees understand and address risk. In this way, ERM fosters an environment of accountability, encouraging all staff to manage risks with diligence. This team-oriented game plan will make risk management a seamless part of day-to-day operations and yield a forward-looking mindset within the organization.

- Better problem-solving: Emergency fixes, legal fees, image repair and other reactive measures cost time and money. You can stifle these issues before they arise with a proactive ERM plan. ERM frameworks use risk assessments to help stop risks before they become larger issues. You can feel prepared to handle uncertainties and seize opportunities in a competitive sector.

- Greater efficiency: Because enterprise risk management for banks can improve resource allocation, it reduces waste while fine-tuning processes. It also refines workflows, giving teams time to focus on core business activities without constant interruptions.

- Data-driven insights: Take advantage of what data can offer to reduce the confusion surrounding risk exposure. Reputable ERM solutions use sophisticated data analytics, automation, reporting tools and cloud computing to deliver insightful details on trends and emerging risks. They can help you improve your strategic planning endeavors so you can make better decisions to meet your business objectives.

- Regulatory preparedness: Compliance audits can be difficult when you don’t have a clear understanding of your risk exposure. With an ERM program in place, you can grasp your true risk profile so that you can prove compliance with confidence. You will also be able to respond to regulatory requests without delay and avoid expensive penalties.

Types of Enterprise Risks for Financial Institutions

No two financial institutions are the same, and the risks they face vary widely. Here are the primary categories of risks addressed within ERM frameworks.

1. Financial Risks

Financial organizations engage in risk management concerning credit, market, liquidity and interest rate volatility. Effective ERM monitors and mitigates these risks to protect assets and profitability.

- Credit risk: This is the risk of a borrower defaulting on their financial obligations. It can affect an organization’s capacity to sustain profitability. Credit risks often need careful monitoring via credit checks and risk assessments. ERM can assist in identifying probable credit risks and creating plans to reduce them.

- Market risk: Market risk is the potential for losses triggered by shifting financial market conditions. Such fluctuations can entail interest rates, exchange rates, stock prices or commodity prices, which all influence asset values and revenue. To reduce the effect, you need tactics like hedging and portfolio diversification.

- Liquidity risk: This is an institution’s capacity to meet short-term fiscal obligations. Ineffective liquidity management can lead to insolvency or other negative consequences. ERM frameworks help institutions anticipate and prepare for liquidity needs, as well as construct backup plans for any shortfalls.

- Interest rate volatility: This connects to liquidity risk. It involves how interest-rate fluctuations can alter a company’s earnings. For instance, rising interest rates can raise borrowing costs. In contrast, falling rates can lower investment returns. In both instances, financial institutions must control their exposure. They can use strategies such as interest rate swaps or fixed-rate loans to manage it.

2. Strategic Risks

Expanding into a new market can be exciting, but without proper market research, it’s easy to overlook key factors like customer demand, local competition, regulatory changes or cultural differences. This can lead to wasted resources and a negative impact on existing revenue streams. Let’s look at some common mistakes.

Mistake Number 1: Launching Goods or Services That Don’t Satisfy Customers’ Needs

Before rolling out a product or service, thoroughly research your target customers’ preferences. Failure to grasp consumer desires exposes your product to low adoption rates and a dissatisfied client base. You risk losing both time and money while damaging your brand’s reputation.

Mistake Number 2: Overinvesting in Experimental Technologies or Strategies

Without question, innovation is a key component of any corporate strategy. But when you sink too much money into new technology or procedures without testing, you’re rolling the dice. If these investments fail to generate the projected ROI, they can siphon resources from other areas of your organization.

Mistake Number 3: Ignoring Market Trends or Competitor Activity

The market changes quickly. When you don’t keep up with trends or competitor tactics, your business may fade into oblivion. That’s because ignoring these shifts could cost relevance and market share. What’s worse, you lose the ability to adjust to new possibilities or obstacles.

3. Compliance Risks

Regulatory compliance is a key component of any financial institution’s risk management program. Non-compliance can result in fines, brand damage or even shuttering the business. The financial industry may face the following issues:

- Increased frequency and complexity of regulatory changes: Regulatory changes are increasing in frequency and complexity. It can be difficult to keep up with new laws that pop up on a regular basis in many sectors. You must be watchful and invest resources in tracking these changes.

- Strain on internal resources to maintain compliance: Many organizations face the challenge of stretching their internal teams too thin. That’s because employees are often required to juggle compliance tasks alongside their core roles. Unfortunately, this pressure often leads to missteps and oversights, severe workplace fatigue and stress among employees.

- High costs associated with maintaining compliance: Compliance often involves hiring specialized personnel or investing in updated systems. Since organizations must conduct regular audits, these costs can add up. Small and mid-sized businesses feel the weight of this even more so.

- Potential for hefty penalties for non-compliance: Ignoring regulations can result in financial penalties, legal backlash and reputational harm. All of these consequences can have long-lasting effects on any business.

4. Operational Risks

Operational risks are any issues that disrupt company operations stemming from processes, people, systems and external events. Operational risks, whether from a failed process or outside issue, can escalate into bigger problems in a short period. Some examples include:

- Data entry errors: Simple mistakes in data entry can snowball into larger issues. Just one accidental keystroke can spell disaster in reporting or customer service. In fact, the Verizon 2023 Data Breach Investigations Report found that 74% of breaches involved a human element. Regular checks and automation can help minimize these errors.

- Third-party risk: Using external vendors for operations can open your business to issues like service delays and security breaches. Vet all third-party vendors with thorough scrutiny. You should also conduct regular audits and have contingency plans in place.

- IT system failures: Technical breakdowns, such as server crashes and network outages, can derail operations. With IT setbacks, you run the risk of delaying services and reducing customer trust. To avoid costly downtime, invest in reliable systems and keep them well-maintained.

5. Cybersecurity Risks

Digital transformation has brought immense benefits to the financial services industry. Nevertheless, it has also exposed it to severe threats. The World Economic Forum’s Global Risks Report 2024 highlighted a 20% year-over-year increase in sophisticated cyberattacks targeting critical infrastructure. Some of the most common ones include:

- Data breaches: Breaches occur when hackers exploit vulnerabilities in a system and expose customer or institutional information. If you experience a data breach, you face monetary loss, compliance penalties and loss in customer trust.

- Phishing and ransomware: These are the most common cyber traps. Both can be detrimental to your operations and bottom line. In phishing, cybercriminals create false emails or webpages that trick users into sharing private information. Passwords and credit card details are examples of sensitive data at risk. Alternatively, ransomware attacks lock up a company’s data. The attackers hold it until the victim pays a ransom.

- Insider threats: Insider threats are security risks instigated by users who misuse their system credentials. Insider attacks can be deliberate or accidental. Either way, they can jeopardize your platforms. Fallout can include data theft and data leaks.

6. ESG Risks

Failing to address ESG risks can lead to loss of stakeholder trust and missed opportunities for sustainable financing.

Environmental Risks

Environmental risks can lead to fines and penalties due to non-compliance with environmental standards. Exceeding emission limits or improper waste disposal are just two examples. These risks can also damage a company’s reputation and lead to higher operating costs.

Social Risks

Negative impacts on the workforce or local communities are examples of social risks.

Examples of social risks include unsafe working conditions, lack of diversity, displacement of local populations or environmental degradation. These issues can lead to protests, compliance problems, lawsuits and brand detriment. Ultimately, if you undergo a social risk, you can face serious litigation, employee attrition, monetary damages and loss of trust from the public.

Governance Risks

Governance risks arise from weak policies or poor management practices within an organization. If these issues continue, checks and balances can fail and unethical behavior may go unchecked.

These problems can harm employees by making the workplace feel unstable. Staff may also face unclear expectations and unfair treatment. Decreased morale, high turnover rates, lower job satisfaction and a distrust of management are a few of the consequences. These risks can also lead to fraud, corruption, a tarnished reputation, or even regulatory investigations.

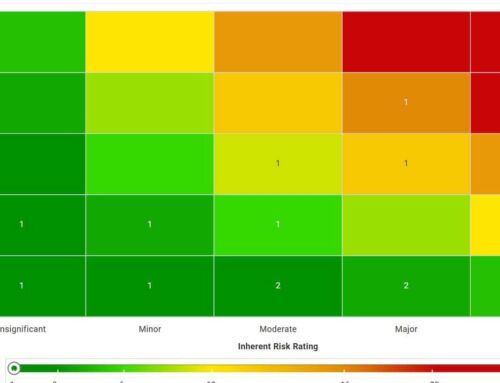

Example of a Data-Driven Approach to Enterprise Risk Management for Financial Institutions

Onspring recently partnered with a financial services organization to develop an ERM strategy. After executing the strategy, the company agreed to conduct a survey with Onspring. The organization’s management team provided the following responses:

Out of 20 responses, a risk’s average score was a 9 (3 – Impact & 3 – Likelihood), but there were three responses that rated that risk as 5 – Impact & 5 – Likelihood. The ERM team could see this position on the heat map and investigate with those individuals.

- Are they in the same department?

- What does that department perceive that the rest of the participants do not?

- Are they in the same management level?

- What needs to be addressed with these three respondents or what needs to be brought to the attention of the rest of the respondents?

As the team continues to think ahead for their ERM program, they intend to add objective measures to the tracked risks, in addition to subjective, opinion-based data already being collected. Tracking incidents, findings and issues and sharing the information across departments will allow them to evaluate (with measurable data) how the identified risks actually play out in business operations. Then, they can communicate high-risk items that may be “under the radar” to stakeholders, as well as assure their employees in cases of perceived high risks that don’t translate to actual events.

This data-driven approach will allow them to take a more proactive stance against risk and strengthen their operations.

Want to see more? Schedule a demo with us any time. We’re happy to talk further about enterprise risk management for financial institutions.